When you look at the facts, it’s clear that Canada is a leader in carbon capture, utilization, and storage (CCUS).

With more than 16 per cent of the world’s CCUS projects currently in operation and a reputation for top notch research, knowledge, and expertise, Canada is a heavy hitter in the carbon tech space.

But, if we are going to continue to lead the world in carbon tech innovation, it’s imperative that we understand Canada’s strengths, gaps, and opportunities across the sector in order to pave the way for emerging innovations, advance technology deployment, and solidify our global leadership position.

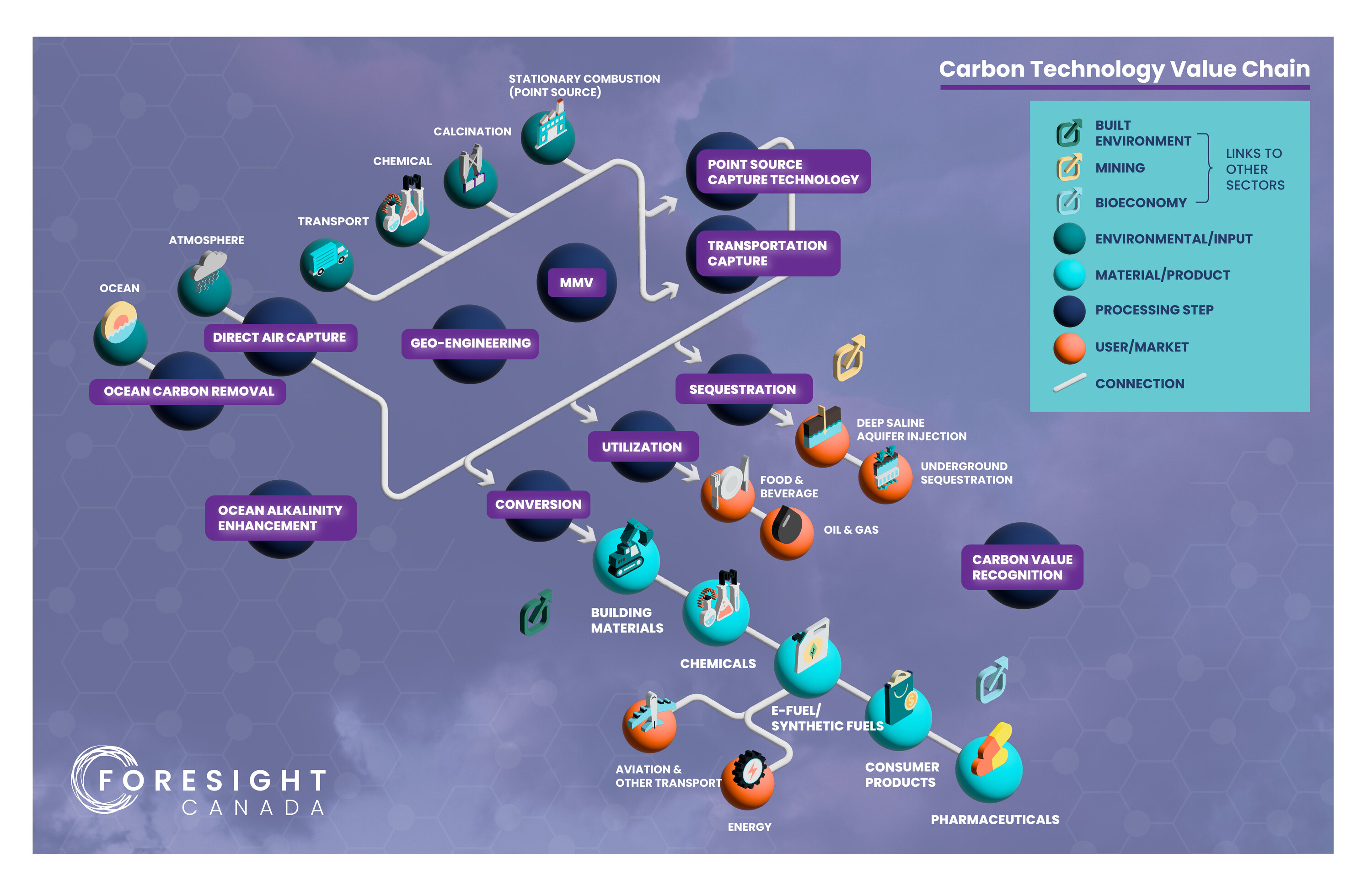

Foresight’s, Canada’s Ventures to Value Chains: Carbon Technology database and report is an all-in-one resource that leverages data from technology companies and other key stakeholders to map, categorize, and analyze strategically important industry value chains for Canada in the clean economy.

An invaluable tool for innovators, industry leaders, investors, academics, and government officials, this resource lists 56 Canadian pure-play carbon tech companies across 9 different value-chain steps, providing key insights into:

- the journey of carbon from emission source to capture and storage, utilization, or conversion;

- the steps taken as carbon is processed, and the ways in which they connect to users, markets, or the environment, and;

- Key strengths, weaknesses, and opportunities across the value chain.

Available for purchase, Canada’s Ventures to Value Chains: Carbon Technology uncovers several key themes that will help guide the future of Canadian carbon tech innovation.

Here’s a preview of some of the key takeaways:

- Alberta has the most carbon tech companies in Canada

- Ontario has some nascent clustering of conversion companies

- Small numbers of measurement, monitoring and verification (MMV) technologies in Canada present an opportunity for innovation as an integral part of CCUS

- Conversion and point source capture have the most number of companies in the Canadian carbon tech value chain

- Conversion technologies are an area of strength in Canada

- Direct air capture is an opportunity for Canada, but ‘brain drain’ is a significant risk

Interested in learning more about Canada’s carbon technology value chain? Check out the Executive Summary.

Scaleable Carbon Management Innovation Starts Here

Scaling carbon management solutions is critical to achieving net zero. Explore the latest insights, technologies, and strategies shaping Canada’s carbon economy and accelerating the commercialization of CCUS innovations.